Buy Now Pay Later apps are popular. Everyone wants to participate in this race to receive the desired stuff and pay for it later. However, getting this function is complex since your credit score, or CIBIL score, is the most important factor. But it is a separate matter. The second most critical step in getting this service is selecting the best Buy Now Pay Later apps. So, we’ve compiled a comprehensive list of the best Buy Now Pay Later apps available. As a result, let’s start with the guide immediately and not increase your concern.

Top 13 Best Buy Now Pay Later Apps You Need To Try

So, here are the best Buy Now Pay Later apps. Read our tutorial carefully to get the most out of them.

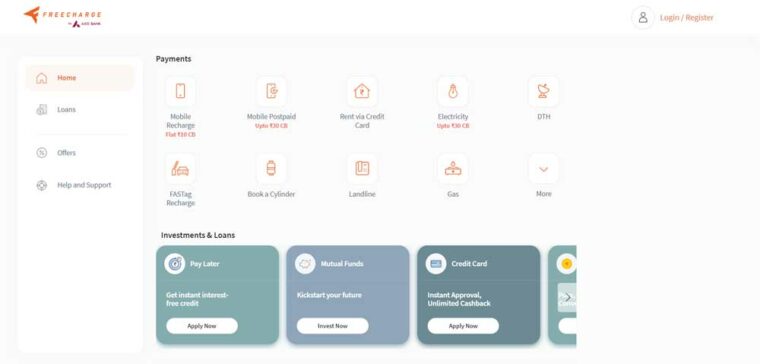

1. FreeCharge

Axis Bank gives Freecharge. Powered by Freecharge, the Buy Now Pay Later option allows users to purchase credit worth Rs 10,000 monthly. Users may make purchases or payments with Freecharge or its merchants or partners using a smooth one-click experience, with the option to repay the balance over 30 days.

If you pick the Buy Now, Pay Later option, you can satisfy all your criteria immediately. If you are short on finances, you may use a pay-later service to purchase things or hire services now and pay for them later. Pay now on Freecharge and later at retailers accepting Freecharge Pay Later for items like mobile, DTH, electricity, landline, broadband, etc. Salaried individuals earning over $10,000 and having a CIBIL score of 720 or above are eligible for the Freecharge Pay Later program.

2. Perpay

Perpay is the best BNPL app for folks with terrible credit since it does not check credit history and instead sets spending limitations based on your verifiable income. Perpay was founded in 2014 and is now based in Philadelphia, Pennsylvania.17 Perpay, with over five million subscribers, was designated the fifth-fastest-growing private company by Inc. magazine in 2019. Customers may shop from over 1,000 top products on the Perpay marketplace. On-time payments increase the typical customer’s credit score by 39 points, providing an advantage over customers with terrible credit seeking to fix it.

3. ZestMoney

There is an increasing trend of buying now and paying later. As a result, consumers are discovering new methods to shop on credit, ranging from apps to credit cards. Furthermore, Zest provides EMIs with 00/0% interest and the option to make payments over 3 to 4 months at no additional cost. Zest allows you to shop at over 10,000 online and 75,000 retail businesses, including Amazon and Flipkart. ZestMoney, a consumer loan fintech company founded in 2016, has grown significantly since its inception. ZestMoney allows you to shop on EMI for free and fast.

You do not need a credit or debit card to use ZestMoney. There is no offline component in Zest. Zero pre-closure fees for Zest loans. If you are in a cash crisis or need a credit history, Zest may assist you if you cannot get financing elsewhere. The technique is straightforward. Install the Zest App, verify your cellphone number, and submit KYC papers to get a credit limit. Zest accepts every payment type. However, EMI plans must be selected and the purchase made. Set up your bank account to automatically repay your debts.

4. Sezzle

Through Sezzle, a company that provides “buy now, pay later” plans, you may pay later on hundreds of goods at stores, including Target, Bass Pro Shops, and Lamps Plus. You may split your purchase into payments instead of paying in full at checkout. There are no interest charges while using Sezzle’s plan, although certain fees may apply. Like Afterpay and Klarna, Sezzle offers BNPL services. BNPL is an economical form of financing, provided you make your payments on time, but it is still a form of debt, and NerdWallet suggests that you pay for non-essential purchases in cash.

Sezzle’s designation as a B Corp distinguishes it from others. Companies that are certified as B Corps must go through rigorous tests and show environmental and social sustainability. To register for Sezzle, you must have a phone number in the United States or Canada and an email address validated with a debit or credit card. Sezzle will establish your first spending limit based on your ability to repay. The company makes approval choices immediately. You can increase your credit limit if you make all your payments on time.

5. Splitit

Splitit is our pick for the best BNPL app with no credit check. Splitit purchases using your current Visa, Mastercard, Discover, or Union Pay credit card rather than establishing new credit. Splitit is a publicly listed company founded in New York City in 2012.15. It has partnered with Wix, Big Commerce, WooCommerce, Shopify, and others to broaden its products. Splitit allows users to use their Visa, Mastercard, Discover, and Union Pay credit cards to earn points on their purchases while paying over time with no interest. Splitit does not charge customers any interest or fees, including late fees. Your credit card company may still charge interest.

6. MoneyTap

MoneyTap’s popular lending platform now includes a new function called Buy Now Pay Later, implemented Wednesday. Users can pay on a flexible timetable when making purchases from different online and offline shops, including 0% EMIs. Recent advancements in the Indian market have resulted in ‘Buy Now Pay Later’ credit. MoneyTap said millennials are using credit options at the checkout line when making large purchases despite the fact that installment loans are not a new concept.

According to the company’s CEO, 10,000 merchants are set to provide 0% and low-cost EMIs via MoneyTap. In addition, the digital lending company plans to develop an EMI card with unique discounts over the next six months. The 0% EMI Pay Later Card has a 30-day interest-free period. Pay later cards enable users to pay partly or in whole after 30 days and then convert the remainder into EMIs after the amount is settled.

7. Paytm Postpaid

Shoppers Stop, Haldiram, Reliance Fresh, Apollo Pharmacy Croma, and Shoppers Stop are stores that accept Paytm Postpaid for groceries, milk, and other household items. Payment history with Paytm impacts your eligibility for both the NBFC and Paytm. You will be requested to furnish Paytm with your transaction history and the payment you made. Additionally, when you seek a credit limit using the app, your CIBIL score will be reviewed. These factors will be considered when awarding credit limits and approvals.

To obtain Paytm Postpaid, you must be at least 18 years old. We will create monthly Postpaid invoices on the first of each month. Every 7th of the month, which is Paytm’s postpaid payment day, you must pay your bill either UPI, Debit Card, or bank account. If you pay your bills regularly, your Paytm postpaid allowance will increase. When you pay back your PAYTM POST purchases, you may also take advantage of EMIs, which allow you to repay the amount in manageable installments without worrying about financial limits.

8. Afterpay

Afterpay has two monthly payment plans and a pay-in-four option. Old Navy, Nordstrom, and Gap are some retailers it partners with. If you pay on time, there are no fees to use Afterpay. It charges a $8 late fee if you miss a payment. Afterpay may perform a light credit check, which will not harm your credit score. As part of the approval process, Afterpay may assess whether you have enough cash on your debit or credit card, how long you’ve been using Afterpay, the purchase amount, and any other outstanding loans with Afterpay.

9. Affirm

Affirm has various BNPL plans, including pay-in-four and monthly payment plans. It partners with big retailers such as Amazon, Walmart, and Expedia. Affirm charges no fees. Also, Affirm may perform a soft credit check, which does not negatively impact your credit. It may also evaluate your past payment history with Affirm, the length of time you’ve had an Affirm account, any notable Affirm loans, your loan use, current debts and income, and any bankruptcies.

10. Apple Pay Later

Apple provides a pay-in-four plan for purchases up to $1,000 at any retailer that accepts Apple Pay online or in-app. Eligible users may apply for Apple Pay Later using the Apple Wallet mobile app. Apple Pay Later has no fees. Apple may conduct a mild credit check as part of the application process. There’s no minimum credit score requirement, although the company claims users with a FICO score of 610 or below may need help being approved. Approval is based on your credit record, purchase data, and any past payment history with Apple Pay Later.

11. PayPal

PayPal provides a pay-in-four and monthly financing option for online purchases. Retailers such as Apple, Home Depot, and Best Buy are among its partners. PayPal does not levy fees. PayPal may conduct a mild credit check. Approval is based on several factors, including your PayPal account history and credit bureau information.

12. Klarna

Klarna provides a pay-in-four plan, a pay-in-30 plan, and monthly financing. Macy’s, Etsy, and Sephora are just a few retailers that sell it. Also, if you use a one-time virtual card at a store that does not work with Klarna, it charges a late cost for missed payments and an unannounced time service fee. Klarna may conduct a mild credit check. According to the company, evaluate credit bureau information, such as whether you’ve made on-time payments on other credit products and obligations you may have.

13. Zip

Zip’s pay-in-four plan is accessible anywhere a Visa is accepted. It also directly partners with Shein, Best Buy, and Fashion Nova businesses. Zip charges an installment cost for the pay-in-four plan, a late fee if missed, and a rescheduling fee if you postpone a payment more than once per calendar month. Zip may perform a mild credit check. Aside from that, the company does not disclose how it authorizes clients, although it claims to employ machine learning, which considers various factors.

Should You Use A Buy Now, Pay Later App?

NerdWallet advocates paying for non-essential purchases in cash wherever feasible. Though BNPL may seem a handy payment option, it remains a debt. When determining whether to apply for a pay-later offer, consider these pros and cons.

Pros

No Interest Financing – Most Buy Now Pay Later apps charge no interest on their pay-in-four loans. This implies that if you make all of your payments on time, you may use the service for free. It is unusual to be able to finance a purchase, particularly a larger-cost item such as a computer, with zero interest.

No Hard Credit Check – Unlike using for a credit card or a loan, Buy Now Pay Later apps do not often conduct a hard credit check, which might temporarily reduce your score. Also, if your credit score could be better, you may have an easier time being approved by a BNPL app than a conventional lender.

Simple, Convenient & Fast Financing Option – Buy Now Pay Later apps are known for simple and easy payment plans. Applications are often incorporated immediately into the checkout process, and approval choices are rapid, allowing you to opt into a BNPL short payment plan in minutes.

Cons

Could Encourage Overspending – BNPL plans might make you feel like you’re spending less than you are. For example, if your purchase budget is $100 and you choose a pay-in-four option, you will only spend $25 upfront. Some consumers may be tempted to return and add additional items to their carts.

Likely Won’t Be Able To Build Credit – Most BNPL providers must consistently report on-time payments to the three major credit agencies. Therefore, you will need help to establish credit with these plans. Nevertheless, they may send past-due accounts to collections, lowering your credit score.

Fees – While some Buy Now Pay Later apps do not impose fees, many do—especially if you miss a payment. Fees may vary from $1 to $15, constitute a considerable proportion of the total, and increase the cost of your purchase.

Customer Service Issues – Some BNPL users may have difficulty setting disputes. For example, if you purchase an item you must return, you must deal directly with the store, even if your loan is with the BNPL lender. This might cause a delay in receiving your refund.

Consider The Following:

Final Thoughts:

This ends our list of the best Buy Now Pay Later apps. Hopefully, you’ll find our advice useful. Furthermore, if you have any queries about our proposed Buy Now Pay Later apps, please leave them in the comments section below.